Readers looking for some encouraging news about the state of the transport sector are probably going to be disappointed. While 2016 was tough and 2017 was even more difficult, things continued to look bleak during 2018. There are a whole host of reasons for this situation – one of the most prominent being Brexit.

Having initially suggested – in April 2018 – that the UK would grow at a rate of 1.6% throughout the year, the International Monetary Fund (IMF) downgraded this prediction a few months later, citing trade tensions and tariff issues as reasons for the revision. Predicted growth for 2019 was set at 1.5%, but this figure was very much dependent on the outcome of Brexit. In November, the IMF warned that a ‘no-deal’ Brexit could cost the UK 6% of GDP.

After an up-and-down year for truck registrations in 2017, the market was not overly confident going into 2018. That trend has continued: figures released by the Society of Motor Manufacturers and Traders (SMMT) in October showed that registrations for trucks in the ’16-tonne and over’ bracket were down 8% for the first eight months of the year (to 27,025). By November, new truck registrations had fallen for the fifth quarter in a row.

Having dipped in 2016-17 to 370,606, the number of HGVs returned to beyond the 2015-16 recorded figure (377,748) in 2017-18. In total, there were 378,476 vehicles on the road, up 7,870 from the previous period. In contrast to the vehicle parc expansion, the number of O licences carried on the pattern of continued decline, dropping 1.2% to 72,547.

There was slightly more positive news in the light commercial vehicle sector. Most favourable was October’s news that new van and pick-up registrations increased by 14.1% over September to 28,494 units. This growth was largely attributed to a rise in large vans (2.5 tonnes to 3.5 tonnes) of 27.6%. However, those figures fit into a larger decline; year-to-date registrations reported at the beginning of November were down 1.6% to 302,741 in 2018.

Also, the RHA’s annual autumn survey ‘Haulage Cost Movement Report 2018’ found that operators saw their costs increase by 3.29% (excluding fuel); by adding fuel into the equation, the figure was 6.31%. Following a now-familiar trend, the cost of fuel continues to rise, and in September broke through the 100ppl barrier.

ECONOMIC BACKDROP

Starting 2018 at 3% in January, the Consumer Price Index (CPI) inflation fell steadily to 2.4% in April, where it remained for most of the year. According to economic analysts, prices slowed for transport and food but rose faster for housing, utilities, recreation and culture during the year.

The UK’s unemployment rate in 2018 also continued a steady downward trend that began in 2016: throughout 2017 unemployment dropped from 4.7% to 4.3%. In June 2018 it fell to 4% (1.36 million unemployed) – the lowest rate the country had seen since 1975. In the period of July to September 2018, there were 32.41 million people in work – 23,000 more compared with the previous quarter and 350,000 more than July to September 2017.

Average earnings (excluding bonuses) went up by 3.1% in the three months to August 2018 compared with a year earlier – rising at their highest pace for nearly 10 years. Average earnings including bonuses rose at a pace of 2.7% in the three months to August, and, in the same month, the Bank of England said it expected total pay rises to climb to a rate of 3.5% by the end of 2020.

August 2018 saw an increase in interest rates for only the second time in a decade. Having risen from 0.25% to 0.5% in 2017, an additional quarter of a percentage point was added in August, meaning the new rate of 0.75% was the highest interest rates had been since March 2009.

VEHICLE ACQUISITION

Results from the RHA costs survey show a trend towards leasing vehicles among members. While nearly three-quarters of members (74.4%) reported that they used purchase or part-purchase methods for their fleets, 51% also said they have started leasing/contract hire arrangements. This figure indicates a major shift in attitudes towards acquisition.

STANDING COSTS: TAXATION

In terms of vehicle excise duty (VED), 2018 is a familiar story to previous years; once again, the chancellor decided to keep HGV rates the same. However, changes are being proposed for 2019, with cleaner HGVs eligible for a small discount, and vehicles with higher emissions paying more.

On 28 March, the RHA spoke out against the announcement from transport minister Jesse Norman regarding pre-Euro VI trucks of 12 tonnes or more being subjected to a 20% increase in road user levy (RUL). The association estimates that by February 2019, some 56% of UK-registered trucks will still fall within this range, and will be faced with an increase; meanwhile those already using Euro VI will see a 10% reduction. For clarification, the current levy of £1,000 will be cut to £900 for Euro VI trucks, but increased to £1,200 for Euro V and older models.

</p>

INSURANCE

Following a reported increase of 2.5% in the 2017 RHA costs survey, the 2018 figure was 6%. The number of providers is shrinking, with on the one hand insurers such as Equity Red Star and Aviva announcing their withdrawal from much of the motor fleet market for haulage, and on the other the insolvency of insurers Enterprise and Lima. The hope is that corrective pricing action by those still in the market should increase stability in 2019.

One piece of welcome news in 2018 was the passing in November of the Civil Liability Bill through the House of Lords. The aim of the Bill is to reform whiplash costs that have added massively to insurance payouts and, therefore, to insurance policies. Royal assent should follow soon and the legislation itself should be in place by 2020.

RUNNING COSTS: FUEL

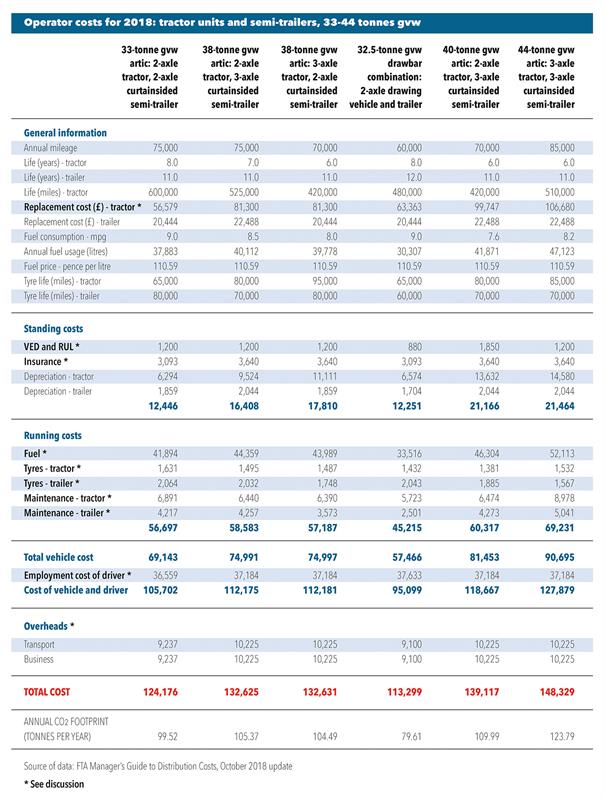

The year didn’t get off to the best start for fuel prices, with Brent oil prices in January hitting a three-year-high of $70 a barrel, and diesel around 98ppl excluding VAT. Reuters and various banks predicted that Brent would average $64-$65 for 2018. As the year went on, so the price of oil and diesel increased, culminating in a point-to-point increase of 11.8%, which adds £4,626 to the cost model per annum, or £89 a week. Adapting those figures to RHA’s benchmark truck – a 44-tonne 6x2 artic combination covering 75,000 miles and returning 8.3mpg – total fuel costs would be £43,725. (For comparison, FTA’s equivalent truck, last column, table p23, travels 85,000 miles at 8.2mpg; its annual fuel costs are estimated to be £52,113.)

Positive news in the autumn budget that fuel duty would be frozen once again (it has remained at 57.95ppl since March 2011), was offset by the announcement of cost increases from the Renewable Transport Fuel Obligation (RTFO). In March, the required fraction of bio content was put up to 7% for diesel, having being less than 5% for many years. From 1 January 2019, the premium was raised further to 8.5% – resulting in an additional cost of about 0.42ppl. Meanwhile, the Advanced (Development) Fuels Mandate, which took effect from the same date, also adds an expected 0.08ppl.

Those using rebated red diesel to power equipment such as fridges were seriously concerned in autumn that the chancellor would remove its tax advantage in the autumn budget, following a call for evidence on whether the use of such fuels contributed to poor air quality. This scenario failed to materialise, so far, at least.

_84c387f2.jpg)

TYRES

The cost of tyres has been a prominent feature of operator costs in recent years, but this was not the case in 2018, despite increasing raw material costs. While there was a drop in demand for conventional tyres, demand for retreaded tyres increased following the European Commission’s introduction in May of a levy on tyres being imported from China. This ‘anti-dumping’ levy is specifically aimed at four Chinese tyre manufacturers, and adds between £45-£75 to the cost of each of their tyres. Another significant moment came in August, when Continental issued a second profits warning for the year.

REPAIRS AND MAINTENANCE

The increase in repair and maintenance costs from the RHA survey – 2.5% – was roughly in line with inflation. In May 2018, the HGV inspection manual was updated due to the European Roadworthiness Directive (2014/45/EC) being transposed into UK law. Although the directive brought changes to some brake testing requirements for centre-axle drawbar trailers manufactured from 1 January 2012, what might have been a costly upgrade eventually proved to be a non-issue, as most met the increased braking efficiency required.

DRIVER EMPLOYMENT AND APPRENTICESHIPS

The driver shortage continues, and isn’t getting any better. The latest RHA estimates suggest as many as 55,000 positions remain unfilled in the industry. With the average age of an HGV driver now 55 – and only 2% of drivers under 25 – the situation shows no signs of changing. Many drivers are coming up to retirement, while clearly not enough young or female drivers are coming through to replace them. In addition, the industry is currently reliant on around 60,000 EU nationals.

Trailblazer apprenticeships and the Apprenticeship Levy, introduced in April and May 2017 respectively, have failed to have the impact expected. This situation reflects all other sectors, with apprenticeship numbers falling since the Levy was announced in 2016. Levy-paying employers, who tend to be the ones taking on apprentices, delayed doing so, to make sure that they would get their money back from the scheme as it was rolled out. That has had the effect of reducing general training in the sector, as budgets are now used only for apprenticeship training. At present, approximately £130 million has been paid into the Apprenticeship Levy by logistics sector businesses, and less than £10m has been drawn back through apprenticeship take up.

DRIVER CPC

The five-year DCPC training deadline is now less than one year away, but in truth it might not even have featured highly on the agenda of some companies which are desperately trying to fill driver positions. There is some concern for what lies ahead, given that the industry is some 10 million DCPC training hours away at present from hitting the target, although that figure does include bus DCPC, too.

OVERHEAD COSTS

While the M6 toll price increased in July, there was good news for users of the Severn Crossing, whose £16.70 crossing charge was eliminated on 17 December 2018.

In other news, in his spring statement, the chancellor announced that the government was bringing forward the next property revaluation for business rates by one year – to 2021.

Non-driving staff wage increases throughout 2018 were mostly near inflation levels. However, electricity cost reports increased by double digits, according to respondents to the RHA survey. Water costs were also ahead of inflation, and lorry parking prices increased, too. In some areas, paid parking has become a must. Many members reported that the cost of telephone and mobile charges, alongside IT maintenance, have been affected by the added burden of trying to keep ahead of scammers and phishers.

THE FUTURE

Within the transport sector, larger companies have started integrating HGVs powered by gaseous fuels, but this is really quite a niche market at present. Smaller electric trucks will no doubt have a part to play in urban environments.

The International Maritime Organisation (IMO) will reduce sulphur quantities from 3.50%m/m (mass by mass) to 0.50%m/m from 1 January 2020. This will add to global demand for clean diesel fuels, and has the potential to increase costs yet again for road diesel.

Back in the UK, the autumn budget brought welcome news of an increase to the annual investment allowance (AIA). The chancellor announced that AIA would rise to £2m from £200,000 fortwo years, and would be available from 1 January 2019 to 31 December 2020. It is aimed at stimulating business investment.

The Brexit cloud continues to hang over the UK, despite promises that the finer details would be clarified by the end of 2018. At the time of writing, no deal had been agreed between parties and a vote on the prime minister’s deal had been delayed from December to January 2019. The levels of uncertainty over which option prevails – a deal, no deal or no Brexit – continues to hamper industry and the effects are likely to be felt in the years to come.